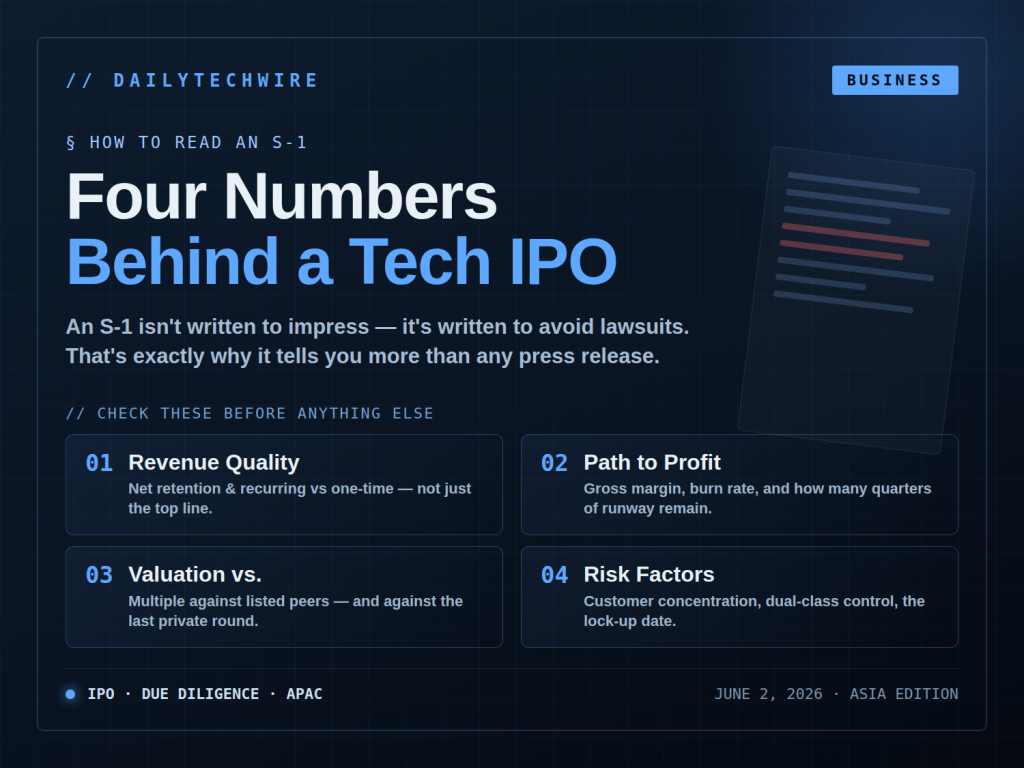

How to Read an S-1: Four Numbers That Decide Whether a Tech IPO Is Worth It

An S-1 is written to avoid lawsuits, not to impress. These are the four sets of numbers analysts check before reading anything else in a tech IPO filing.

How to Read an S-1: Four Numbers That Decide Whether a Tech IPO Is Worth It

An S-1 isn’t written to impress. It’s written to avoid lawsuits. That’s why an IPO document usually reveals more than any press release from the same company. The shareholder letter up front may be full of inspirational language, but it’s the “Risk Factors” section and the audited financial statements where the real story lies.

For investors and founders in APAC tracking the tech IPO window, knowing how to read a filing matters more than knowing how to read the headlines about it. The framework below focuses on four sets of numbers that analysts check before reading anything else.

Revenue structure, not just the top-line number

The first number everyone looks at is revenue. The more important number is the quality of that revenue. A SaaS company announcing strong ARR growth may be masking high churn by upselling to existing customers. The net revenue retention rate, if disclosed, tells you whether existing customers are spending more or less over time. Below 100% is a sign the business is leaking.

You need to separate recurring revenue from one-time revenue. Two companies reporting the same growth rate can have completely different risk profiles if one lives on MRR while the other lives on non-repeating project contracts.

The path to profitability, or the absence of one

Gross margin tells you whether the business model is structurally capable of turning a profit. A software company with a 75% gross margin has entirely different room to maneuver than an e-commerce company at 25%. Operating margin and EBITDA tell you how far it still is to break-even.

What to check: burn rate and runway. A filing that reveals a company burning cash fast and going public to replenish capital is a very different signal from a company going public from a self-funded position. The remaining cash divided by the quarterly loss gives you the number of quarters left if no new capital comes in.

Valuation relative to what

A valuation only means something when placed next to a comparable. The company’s EV/sales or P/E needs to be measured against listed peers in the same industry. If a company asks for a multiple double that of a direct competitor without double the growth, that’s a question to raise, not a reason to get excited.

The second comparison matters just as much: the IPO valuation versus the most recent private round. An IPO priced below the previous round, a public down round, says something about how the private market once mispriced it. The cap table in the S-1 tells you who put in capital, at what level, and how much they’ll be diluted after listing.

What the filing is forced to admit

The “Risk Factors” section is often skipped because it’s long and seems boilerplate. That’s a mistake. The language is required to include generic risks, but the company’s own specific risks—a single customer accounting for most of the revenue, a pending lawsuit, dependence on a third-party platform—are where the real risks get disclosed for legal reasons.

A dual-class share structure, if present, tells you how much control remains in the founders’ hands after the IPO. The lock-up period tells you when insiders are allowed to sell, a date that often creates pressure on the price later on.

An Asian capital perspective

For Southeast Asian and Indian tech companies weighing a U.S. listing over a domestic exchange, the S-1 becomes a rare window into how cross-border capital actually values regional assets. APAC investors read these filings not just to assess a single deal, but to recalibrate multiple expectations across their entire portfolio of private, unlisted companies.

A filing doesn’t answer the question of whether the stock will go up or down. It answers a humbler and more useful question: are the numbers consistent with the story. When the two diverge, the numbers are usually right.