Japan and Korea Are Quietly Reorganizing Their Chip and Robotics Playbooks

Japan and Korea keep being framed as chip and robotics rivals, but their supply chains are wired into each other in ways the rivalry narrative misses.

In a Tokyo office tower last year, a procurement manager for a robotics firm described his sourcing map without much drama: photoresist and etching gases from Japanese suppliers, memory modules and display panels from Korean fabs. That casual division of labor captures something the headlines about rivalry often miss. Japan and Korea do not simply compete in semiconductors and robotics. Their supply chains are wired into each other.

Two strengths, pointed in different directions

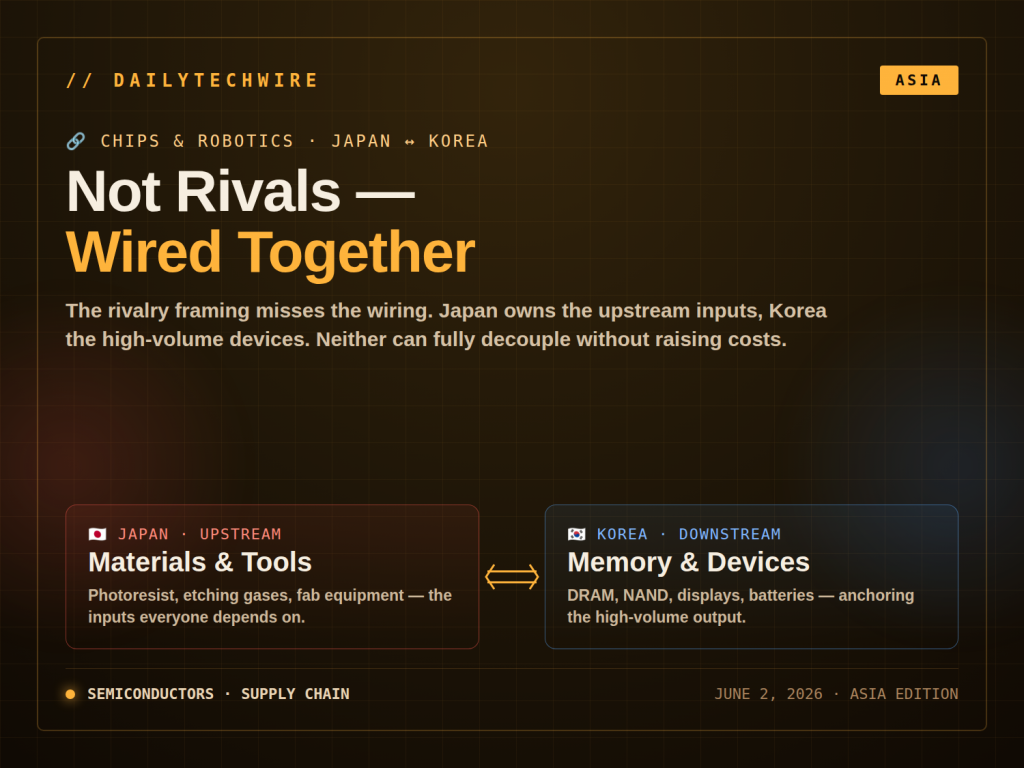

Japan's advantage in the chip world sits upstream. The country's firms hold large shares in semiconductor materials and manufacturing equipment, the unglamorous inputs that fabs everywhere depend on. The 2019 export-control episode, when Tokyo tightened shipments of key chemicals to Korean buyers, demonstrated how much leverage sits in that position, and how disruptive it can be when the relationship sours.

Korea's strength sits closer to the finished product. Its memory manufacturers anchor a significant slice of the global DRAM and NAND markets, and the country's display and battery industries feed the same export engine. The contrast is straightforward: Japan tends to dominate the toolmaking and inputs, Korea the high-volume devices.

That asymmetry is why the two countries keep ending up at the same table even when politics pushes them apart.

Robotics is where the gap is narrower

Industrial robotics tells a different story. Japan has been a long-standing center for industrial robot manufacturing, with companies whose arms populate factory floors across the region. The expertise runs deep in precision motion control and the components that go into it.

Korea's robotics push has leaned toward deployment and integration, often inside its own manufacturing and consumer-electronics conglomerates. The result is two ecosystems that look similar from a distance but differ in emphasis: one rooted in building the machines, the other in putting them to work at scale and increasingly in service and humanoid prototypes.

Aging demographics give both countries a domestic reason to accelerate. Shrinking workforces make automation less a productivity luxury and more an operational necessity, particularly in manufacturing-heavy economies.

The cross-border dynamic that matters

The interesting layer is not who wins but how the dependency reshapes decisions. When trade friction flared, Korean firms moved to localize parts of their materials supply and diversify away from single-country reliance. Those efforts reduced exposure but did not erase it, because the technical lead in some specialty materials remains concentrated in Japanese hands.

Government policy on both sides has pushed toward domestic capacity in strategic segments, echoing a global pattern of subsidy-backed reshoring seen in the United States and Europe. The local nuance is that neither Japan nor Korea can fully decouple from the other without raising costs and slowing output, which keeps the commercial relationship intact beneath the diplomatic noise.

What to watch

The near-term questions are practical rather than dramatic. How far do Korean memory makers go in securing alternative materials sources? Does Japan convert its equipment and materials lead into a larger role in advanced packaging, an area drawing heavy investment as chipmakers chase performance gains without smaller transistors? And does robotics become a genuine area of collaboration, given that both face the same labor math?

The answer will be shaped less by any single announcement and more by how procurement managers like the one in Tokyo redraw their sourcing maps over the next several years.